by Zoltan Hovanyecz | Oct 19, 2018 | Florida Insurance, Hurricane Irma, Property Damage

Hurricane. Fire. Water. No business wants to shut down from a natural or man-made disaster. When disaster happens, will you be ready to ensure the continuity of your business?

Hurricane. Fire. Water. No business wants to shut down from a natural or man-made disaster. When disaster happens, will you be ready to ensure the continuity of your business?

Insurance for your business consists of many aspects, the major one being business interruption. Business interruption is recovery for lost business income while your business is non-operational as a result of a covered insurance claim. While the protection from this type of coverage is invaluable, business interruption must be purchased in addition to your standard business insurance policy. Having business interruption coverage keeps you protected for lost profits during downtime.

Business interruption typically covers the period beginning when the company operations have ceased or been reduced due to a loss which is covered by the insurance policy (such as a hurricane) through the time that business operations have returned to pre-loss condition. Insurance companies label this time as the “period of restoration.” There are limits on how long a business can be in the “period of restoration” while policy benefits continue to be paid. In other words, you don’t have an unlimited amount of time to rely on your business interruption coverage bring your business back to full operational capacity after a loss.

Business interruption will also cover a limited amount of extra expenses incurred during the period of restoration that are deemed necessary. For example, if you have to hire additional staff to meet production demands due to equipment breakdown after a loss, extra expense would cover this. As with everything else, there are limits to extra expense recovery.

THINGS TO KEEP IN MIND WHEN ASSESSING YOUR BUSINESS INSURANCE PLANS:

Have a good accountant and keep great records.

Keeping an accurate record of your businesses’ accounting is the most important aspect of your business insurance plan. Accounting is important because you are going to need to provide calculations to the insurance company to justify your lost business income. The better your records, the easier it will be to prove your losses and will give you the best chance to recover 100% of your policy benefits.

Take an inventory before and after a loss.

Assuming you are already keeping great records, your inventory and stock is being updated regularly. Assuming you have time to prepare before a known disaster, get an accurate inventory before time runs out. Once you are able to get back into your business after the loss, you will need to account for the damaged and non-damaged inventory.

Have a post-disaster plan.

If you run a business that is dependent on utilities (water, power, internet, etc.), you should have a plan on how to restore those valuable utilities to your business as quickly as possible to prevent unnecessary losses after a disaster. Keep in mind that many policies have limits or exclusions on spoilage.

Having proper insurance coverage, accounting, documentation, and photographs can help ameliorate stressful situations. If you have any questions regarding your business coverage, don’t hesitate to give us a call.

by Zoltan Hovanyecz | Oct 6, 2017 | Florida Insurance, Hurricane Irma, Property Damage

Now that we are a few weeks removed from Hurricane Irma’s impact, most Florida citizens who sustained property damage have already reported their claims to their insurance companies. With the huge volume of Hurricane Irma claims, it’s likely that most insureds have not yet received a claims decision or even a payment from their insurance company.

As those claim payments start coming in, the important question is how do you know if the insurance company reimbursed you for the full amount of damages that your property sustained?

There are a few things to keep in mind when receiving that first check from your insurance company:

- Hurricane Deductible: Insurance policies carry larger deductibles for damages resulting from a Hurricane. Hurricane deductibles are typically 2% or 5% of the total amount of insurance coverage. In comparison to your typical $1,000.00 deductible, you could have up to a $15,000.00 deductible (at 5%) on a $300,000.00 insurance policy. If your insurance company is going to make payment, you won’t have to pay your deductible to anyone, but the amount your insurance company pays you will be reduced by your deductible. Keep your deductible in mind when assessing your damages as you may not have enough damage to meet your deductible.

- Documenting Damages: Pictures, pictures, pictures! Take as many photographs and videos of all of the damage inside and outside of your home. This includes fallen debris, water stained walls or ceilings, actual water on surfaces, wet baseboards, missing roof tiles, etc. Down the road, when the insurance company wants to avoid payment, it will be critical to show in photographs where you sustained damages as a result of the storm.

- Roof Damage: If you have sustained damage to your roof, make sure that a qualified and licensed roofer inspects and documents the hurricane damage to your roof. Get an estimate for a roof replacement or repairs. If you have leakage on the interior, make sure to have a tarp installed on your roof until repairs can be made.

- Hidden Damage: Damages may have occurred in places that are not readily visible to you—inside walls, in the attic, underneath roof tiles or shingles, behind cabinets, etc. Water will follow the path of least resistance and damage may not become evident until weeks or months after the storm. You can expect to discover more damages when you begin making repairs and opening walls.

- Signing a Release: The insurance company may offer you money in exchange for signing a Release. A Release typically precludes you from receiving any more money from your insurance company for your claimed damages. It precludes you from submitting supplemental claims to your insurance company and you also give up your right to sue your insurance company. If you sign a Release and find hidden damage down the road, you will not be able to get any more money. Releases are very serious. Do not sign a release from an insurance company unless you have consulted with an attorney.

If you’ve received a payment from your insurance company for Hurricane Irma damages, feel free to give us a call for a free claim evaluation. More likely than not, the insurance company did not pay you what you are entitled to under your insurance policy.

Your Property Damage, Our Problem!

by Zoltan Hovanyecz | Sep 7, 2017 | Florida Homeowners Insurance, Florida Insurance, Hurricane Irma, Property Damage

As we all prepare for Hurricane Irma, and after you have made sure you and your family are safe, it is important to take some quick steps to ensure that once Hurricane Irma passes, any hurricane related damage to your home or business is promptly reported to your insurance company, assessed, inspected by your insurer and other professionals, repaired by a reputable contractor, and ultimately paid for in full by your insurance company (less your deductible of course).

The Florida Justice Association has put together a great list of tips you should keep in mind to ensure everything with your insurance company goes smoothly after the storm. Keep in mind that immediately after the hurricane, there will be people out here looking to take advantage of our desperate citizens.  This is why one of the most important post-storm tips is to know exactly who you are dealing with and what you are signing before you enter into any agreements with anyone. Be careful of anyone who tells you not to worry about the cost of their services because your insurance company will pay for it. The bottom line is: do not sign anything you are not 100% certain about without first consulting an attorney familiar with the handling of property insurance claims.

This is why one of the most important post-storm tips is to know exactly who you are dealing with and what you are signing before you enter into any agreements with anyone. Be careful of anyone who tells you not to worry about the cost of their services because your insurance company will pay for it. The bottom line is: do not sign anything you are not 100% certain about without first consulting an attorney familiar with the handling of property insurance claims.

We hope that insurance companies will be quick, fair, and reasonable in adjusting Hurricane Irma claims, but there will inevitably be issues. We will be here after Hurricane Irma to provide legal advice and representation to our fellow Floridians affected by the storm and dealing with their insurance companies. We hope that the storm’s impact is minimal, but property damage is almost a certainty and you should ensure your property interests are protected, both before and after the Hurricane Irma.

Your Property Damage, Our Problem!

by Zoltan Hovanyecz | Nov 4, 2015 | Florida Homeowners Insurance, Florida Insurance

All Florida homeowners insurance policies carry a deductible usually ranging from $500 to $2,500. Just like an auto insurance policy, the deductible is the policyholder’s financial responsibility for a portion of the damages in the case of an insurance claim. Unfortunately, deductibles have led to some confusion among policyholders deciding if they should file an insurance claim.

Occasionally, I hear concern from policyholders who tell me that they don’t want to file a homeowners insurance claim because they don’t have the money to pay their deductible or are concerned about having to come out of pocket for the deductible. With a $2,500 deductible, it would be impossible for some families to meet this financial burden, especially when faced with potentially other costly repairs and damages to the their home stemming from the insurance claim. However, it’s important for policyholders to understand that under a typical Florida homeowners insurance policy, you do not have to pay your deductible to the insurance company in the event of an insurance claim; the amount of your deductible is simply reduced from the total payment issued to you by the insurance company for the damages to your home.

For example, if you suffer a plumbing leak that causes $20,000 of damage to your home, and you have a $2,500 deductible, your insurance company would issue you payment in the amount of $17,500. You do not have to pay the insurance company your $2,500 deductible. In fact, you do not have to come out of pocket at all as long as you can find someone to make complete repairs to your property with the amount of money paid by the insurance company. Whether the insurance company paid enough to begin with is another issue previously discussed here.

There are however certain circumstances where the payment of your deductible can change. Depending on your insurance company, you may have an insurance policy that provides the insurance company with the “right to repair” or “option to repair” your home as previously discussed in our blog post entitled “The Insurance Company’s Right to Repair and Option to Repair; What are Your Rights and Options?” If your insurance company utilizes this process, rather than paying you directly for the damages to your home, the insurance company will choose and send their own contractor to make repairs to your home. The insurance company then pays their chosen contractor directly for the cost of repairs. In this situation, depending on your insurance company, you may be obligated to pay your deductible directly to the insurance company’s contractor before the work begins.

If you or anyone you know has questions about insurance policy deductibles, do not hesitate to contact us.

by Zoltan Hovanyecz | Sep 30, 2015 | Florida Homeowners Insurance, Florida Insurance

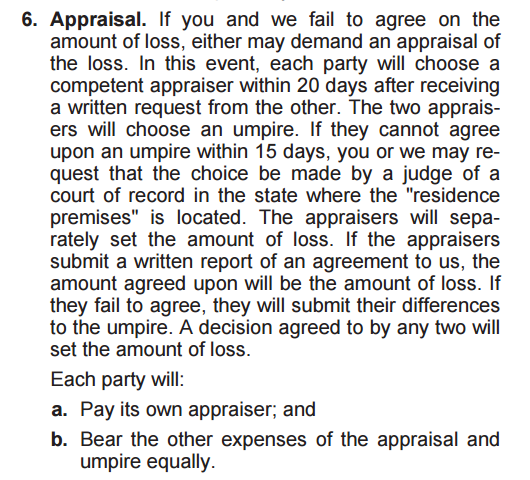

Many Florida homeowners insurance policies contain a specific clause called appraisal which can have a huge impact on the outcome of your homeowners insurance claim. Most homeowners have no idea that an appraisal clause exists in their insurance policy and find out for the first time when their insurance company demands appraisal of their homeowner’s insurance claim. To get an idea of what you are looking for, a typical appraisal clause looks similar to this:

These appraisal clauses are nearly identical between most Florida homeowners insurance policies and can be used by either the homeowner or insurance company to determine the total amount of damage to the home. However, before a claim can be submitted to appraisal, the homeowner and insurance company must have a disagreement regarding the dollar amount of damage to the home. For example, if the insurance company decides that a plumbing leak has caused $5,000 of damage to your home but your contractor gives you an estimate of $20,000 to make repairs, the insurance company is entitled to demand appraisal to determine what the insurance company is obligated to pay you for your damages. Ultimately, this may result in you receiving less than the $20,000 it will cost you to make repair the damage.

The appraisal process requires that the homeowner and insurance company each select their own appraiser to represent them. The appraisers will then try to come to a mutual agreement as to the damages to the home. If they are able to agree, the final number will fall somewhere between the damages determined by your or your contractor and those determined by the insurance company. If the appraisers cannot reach an agreement, the appraisers are required to select a neutral umpire who will then make the final determination as to the amount of damages. The number arrived at via appraisal is FINAL and outside of very specific circumstances, cannot be challenged or circumvented.

Even in light of the nature of appraisal, is not necessarily a bad thing. Given the right circumstances, appraisal can be a benefit to the policyholder. In other circumstances, where appraisal may not be preferred, certain actions can be taken to avoid appraisal. If you have any questions about appraisal or about your claim in general, please don’t hesitate to contact us.

by Zoltan Hovanyecz | Aug 26, 2015 | Florida Insurance, Property Damage

Although you can never prepare for an insurance company’s dishonest tactics, you can certainly make sure you’ve done everything in your control to ensure the best chance of a fair and prompt resolution to your insurance claim stemming from hurricane damage to your home or business. This post will discuss the steps you can take before a hurricane strikes that will put you in the best position to recover the full amount of damages from your insurance company. The National Hurricane Center and a number of other sites have extensive guides on how to personally prepare your home and family for a hurricane so this post will only discuss the insurance aspect of hurricane preparedness.

Check Your Insurance Policy

Before you can even file a claim, you need to make sure you have the appropriate insurance policy and sufficient coverages. This includes making sure you have:

- Enough dollar amount of coverage under the dwelling portion (Coverage A) of your insurance policy to replace your entire home or business in case of a total loss. Too often when reviewing insurance policies I find that some clients do not even know that they are underinsured.

- Enough coverage for your personal property and scheduled items keeping in mind that typical insurance policies have very low limits for jewelry and collectibles unless you have specifically paid for scheduled or itemized coverages.

Document Your Home and Personal Property

When you file a claim with your insurance company, it would be helpful to show the condition of your home or business prior to the damage. Similarly, if you sustain damage to your personal property, the insurance company will want to see the condition and existence of the personal property prior to the damage.

I’ve found that the most efficient way of documenting personal property is by taking a video. This is very easy to do on your cell phone and can take as little as a few minutes to simply walk around your home documenting your personal property while narrating the descriptions. You can even store your video remotely on a cloud based service like Dropbox or iCloud should your phone become damaged or lost.

Have Your Home and Property Inspected

Insurance companies often deny claims saying that the damage is preexisting damage so it’s important to document the condition of your home prior to sustaining damage, especially your roof and interior finishes, showing that there are no current leaks or damage. Also have the rest of your home inspected and documented including screened enclosures, fences and air conditioning systems.

Know Who to Call When Disaster Strikes

Once you sustain damage to your home or business, depending on the severity, you should be prepared to call someone you trust to prevent any further damage to your home and to make temporary repairs. For example, if you sustain damage to your roof, you should be prepared to put a tarp on your roof. If you sustain water damage on the inside of your home, be prepared to call someone who can remove the water. And when you are ready to file an insurance claim, you should have someone you trust who you can call to handle your insurance claim for you.

If you have any questions on preparing your home or business for a hurricane or if you have suffered hurricane damage in Broward, Palm Beach, or Miami-Dade County, contact us for guidance or information.

For information on how to personally prepare yourself or family, a good resource is the National Hurricane Center’s hurricane preparedness guide which can be found here.