by Zoltan Hovanyecz | Sep 7, 2017 | Florida Homeowners Insurance, Florida Insurance, Hurricane Irma, Property Damage

As we all prepare for Hurricane Irma, and after you have made sure you and your family are safe, it is important to take some quick steps to ensure that once Hurricane Irma passes, any hurricane related damage to your home or business is promptly reported to your insurance company, assessed, inspected by your insurer and other professionals, repaired by a reputable contractor, and ultimately paid for in full by your insurance company (less your deductible of course).

The Florida Justice Association has put together a great list of tips you should keep in mind to ensure everything with your insurance company goes smoothly after the storm. Keep in mind that immediately after the hurricane, there will be people out here looking to take advantage of our desperate citizens.  This is why one of the most important post-storm tips is to know exactly who you are dealing with and what you are signing before you enter into any agreements with anyone. Be careful of anyone who tells you not to worry about the cost of their services because your insurance company will pay for it. The bottom line is: do not sign anything you are not 100% certain about without first consulting an attorney familiar with the handling of property insurance claims.

This is why one of the most important post-storm tips is to know exactly who you are dealing with and what you are signing before you enter into any agreements with anyone. Be careful of anyone who tells you not to worry about the cost of their services because your insurance company will pay for it. The bottom line is: do not sign anything you are not 100% certain about without first consulting an attorney familiar with the handling of property insurance claims.

We hope that insurance companies will be quick, fair, and reasonable in adjusting Hurricane Irma claims, but there will inevitably be issues. We will be here after Hurricane Irma to provide legal advice and representation to our fellow Floridians affected by the storm and dealing with their insurance companies. We hope that the storm’s impact is minimal, but property damage is almost a certainty and you should ensure your property interests are protected, both before and after the Hurricane Irma.

Your Property Damage, Our Problem!

by Zoltan Hovanyecz | Nov 4, 2015 | Florida Homeowners Insurance, Florida Insurance

All Florida homeowners insurance policies carry a deductible usually ranging from $500 to $2,500. Just like an auto insurance policy, the deductible is the policyholder’s financial responsibility for a portion of the damages in the case of an insurance claim. Unfortunately, deductibles have led to some confusion among policyholders deciding if they should file an insurance claim.

Occasionally, I hear concern from policyholders who tell me that they don’t want to file a homeowners insurance claim because they don’t have the money to pay their deductible or are concerned about having to come out of pocket for the deductible. With a $2,500 deductible, it would be impossible for some families to meet this financial burden, especially when faced with potentially other costly repairs and damages to the their home stemming from the insurance claim. However, it’s important for policyholders to understand that under a typical Florida homeowners insurance policy, you do not have to pay your deductible to the insurance company in the event of an insurance claim; the amount of your deductible is simply reduced from the total payment issued to you by the insurance company for the damages to your home.

For example, if you suffer a plumbing leak that causes $20,000 of damage to your home, and you have a $2,500 deductible, your insurance company would issue you payment in the amount of $17,500. You do not have to pay the insurance company your $2,500 deductible. In fact, you do not have to come out of pocket at all as long as you can find someone to make complete repairs to your property with the amount of money paid by the insurance company. Whether the insurance company paid enough to begin with is another issue previously discussed here.

There are however certain circumstances where the payment of your deductible can change. Depending on your insurance company, you may have an insurance policy that provides the insurance company with the “right to repair” or “option to repair” your home as previously discussed in our blog post entitled “The Insurance Company’s Right to Repair and Option to Repair; What are Your Rights and Options?” If your insurance company utilizes this process, rather than paying you directly for the damages to your home, the insurance company will choose and send their own contractor to make repairs to your home. The insurance company then pays their chosen contractor directly for the cost of repairs. In this situation, depending on your insurance company, you may be obligated to pay your deductible directly to the insurance company’s contractor before the work begins.

If you or anyone you know has questions about insurance policy deductibles, do not hesitate to contact us.

by Zoltan Hovanyecz | Sep 30, 2015 | Florida Homeowners Insurance, Florida Insurance

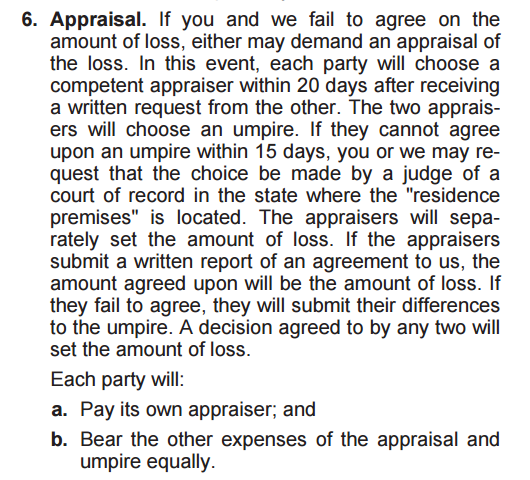

Many Florida homeowners insurance policies contain a specific clause called appraisal which can have a huge impact on the outcome of your homeowners insurance claim. Most homeowners have no idea that an appraisal clause exists in their insurance policy and find out for the first time when their insurance company demands appraisal of their homeowner’s insurance claim. To get an idea of what you are looking for, a typical appraisal clause looks similar to this:

These appraisal clauses are nearly identical between most Florida homeowners insurance policies and can be used by either the homeowner or insurance company to determine the total amount of damage to the home. However, before a claim can be submitted to appraisal, the homeowner and insurance company must have a disagreement regarding the dollar amount of damage to the home. For example, if the insurance company decides that a plumbing leak has caused $5,000 of damage to your home but your contractor gives you an estimate of $20,000 to make repairs, the insurance company is entitled to demand appraisal to determine what the insurance company is obligated to pay you for your damages. Ultimately, this may result in you receiving less than the $20,000 it will cost you to make repair the damage.

The appraisal process requires that the homeowner and insurance company each select their own appraiser to represent them. The appraisers will then try to come to a mutual agreement as to the damages to the home. If they are able to agree, the final number will fall somewhere between the damages determined by your or your contractor and those determined by the insurance company. If the appraisers cannot reach an agreement, the appraisers are required to select a neutral umpire who will then make the final determination as to the amount of damages. The number arrived at via appraisal is FINAL and outside of very specific circumstances, cannot be challenged or circumvented.

Even in light of the nature of appraisal, is not necessarily a bad thing. Given the right circumstances, appraisal can be a benefit to the policyholder. In other circumstances, where appraisal may not be preferred, certain actions can be taken to avoid appraisal. If you have any questions about appraisal or about your claim in general, please don’t hesitate to contact us.

by Zoltan Hovanyecz | Jul 24, 2015 | Florida Homeowners Insurance, Florida Insurance

In Florida, most homeowners insurance policies contain a clause stating how soon a policyholder is required to report their insurance claim to the insurance company. Although each insurance policy differs slightly regarding notice to the insurance company, most policies consist of essentially the same reporting requirement. When a loss occurs a policy holder must:

give prompt notice to us or our agent

For example, during hurricane Wilma, many policyholders suffered damage to their roofs that was not immediately noticeable so these policyholders did not file insurance claims. It is not until sometime later that the policyholder’s roof would begin to leak from the damage caused by the hurricane. Because of this, some policyholders first reported their hurricane Wilma claim to their insurance company months and sometimes years after hurricane Wilma came through Florida. These “late reported” claims resulted in years of litigation in Florida Courts regarding what constitutes “prompt” notice and whether the insurance company is required to pay for the insurance claim when the notice is not “prompt.”

Reporting of Non-Hurricane Related Insurance Claims

For typical property insurance claims that do not result from hurricane damage, such as plumbing leaks, fires, drain backup, etc., “prompt” has been interpreted by Florida courts, in the most simplest sense, to mean that you must report your claim such that the insurance company is not prevented from conducting a full independent investigation and determination of coverage for your insurance claim under your insurance policy. Florida courts typically refer to this concept as “prejudice”, and depending on how “prompt” your reporting was, prejudice may be presumed against you and you may be required to prove that the reporting of your insurance claim did not “prejudice” the insurance company. For a full discussion of the legal standard for “prejudice”, you can read the Third District Court of Appeals case of Hope v. Citizens Property Insurance Corporation here. Some of the things that may considered “prejudicial” to the insurance company are:

- Repairs made to the home such that the insurance company cannot inspect the damages that existed at the time of the loss

- Discarding plumbing parts, pipes, or damaged building materials making them unavailable for inspection by the insurance company

- Failing to protect the property from additional damage resulting in further damage that makes it impossible for the insurance company to inspect the damages as they existed at the time of loss

Although these factors may make it more difficult to recover from the insurance company, they do not necessarily preclude you from doing so. Contact us for a free evaluation of your claim.

Reporting of Hurricane Related Insurance Claims

Since hurricane Wilma, the Florida legislature has created Fla. Stat. § 627.70132 which specifically address the time in which an insurance claim involving damage from a hurricane must be reported to the insurance company:

A claim, supplemental claim, or reopened claim . . . for loss or damage caused by the peril of windstorm or hurricane is barred unless notice of the claim . . . was given to the insurer . . . within 3 years after the hurricane first made landfall or the windstorm caused the covered damage.

If you have any questions about your insurance claim, please contact us.

by Zoltan Hovanyecz | May 15, 2015 | Florida Homeowners Insurance

This post discusses homeowners insurance policyholders’ rights, options and obligations when their homeowners insurance carrier invokes its right to repair (also known as option to repair) for a property damage insurance claim in Florida. Some of the Florida insurance companies currently engaging in the right to repair is People’s Trust, Florida Peninsula Insurance Company, Heritage Property and Casualty Insurance Company, and Prepared Insurance Company. Although the concept of right to repair has been around for quite some time, it is only in recent years that Florida insurance companies have begun making this process part of their everyday business practice.

When an insurance company invokes the right to repair, the insurance company repairs the damages caused to your property by using their own contractor or repairmen. In contrast, on a typical insurance claim where the right to repair is not invoked, the insurance company will just pay the policyholder directly for the dollar value of damage caused to the property. In typical insurance company fashion, by using their own contractors and repairmen, the insurance company can put more money in their own pockets rather than paying it to their policyholder. However, many times the right to repair process can result in:

- substandard repairs

- partial repairs such as resurfacing of materials rather than replacing with new materials

- a total lack of control over the repairs being performed by the insurance company

- unlawful repairs and repairs performed without permits

- lost time while the policyholder has to stay at home to monitor the insurance company’s repairs

Before agreeing to allow your insurance company to repair your property after a loss, it is important to know your legal rights and to make sure the repair is being performed properly and lawfully. If your insurance company has invoked the right to repair for your insurance claim, it is extremely important that you do not sign any documentation presented to you by the insurance company without first talking to an attorney and discussing your rights under your insurance policy.

At Schatzman & Hovanyecz, P.A. we are experienced in handling and litigating right to repair cases successfully, and many times we are able to secure a cash payment rather than allowing the insurance company to repair your home. Contact us for a free consultation regarding your right to repair insurance claim.

by Zoltan Hovanyecz | Apr 21, 2015 | Florida Homeowners Insurance

Do you know what your homeowners insurance policy actually covers?

You call your insurance agent, fill out an application, pay your premiums and years go by without any problems. So there’s no need to review your insurance policy or ask any questions, right?

Unfortunately, if the time comes when you do have to report a claim to your insurance company, before you pick up that phone, it’s important to know that your claim will be covered by your insurance policy. If you do not have the proper insurance policy in place before your loss, there is generally nothing you can do to correct this after damage occurs to your home.

It’s all too common that we run into policyholders who have to pay out of pocket for thousands of dollars of damage because they are either under-insured or have no coverage at all under their homeowner insurance policies. Some of the more surprising examples are insurance policies that only provide $1,000 of coverage or policies that totally exclude water damage. There are also other insurance policies known as “named perils” policies that only provide coverage for a limited number of losses such as fire, theft, volcanoes, and others. Under these types of policies, there is generally no coverage for water damage, plumbing failures, or hurricanes. This can be a major problem when a policyholder realizes this for the first time after reporting their claim to their insurer.

Many times, all it takes to get your policy in check is a quick call to your insurance agent. He or she will be able to answer your questions about what exact type of insurance policy you have and the different types of coverages afforded to you under your policy. Some questions you should ask your agent are:

- What type of policy do I have (H-03, H-06, H-08, etc.)?

- What are my policy limits?

- Do I have coverage for water damage?

- What are the limits to additional coverages (mold, ALE, etc.)?

- Will my current insurance company exercise their right to repair my home in the case of a covered loss?

Ask your agent to explain how the answer to each of these questions affects the coverage afforded to you under your current insurance policy. If you still have questions about your coverage, please contact our office and we will be happy to help.